[OC] House price you can afford by paying 1000/month for 30 years vs. interest rate

[OC] House price you can afford by paying 1000/month for 30 years vs. interest rateSubmitted by hmiamid t3_xy7qym in dataisbeautiful

burn-it-all- t1_irfwiqh wrote

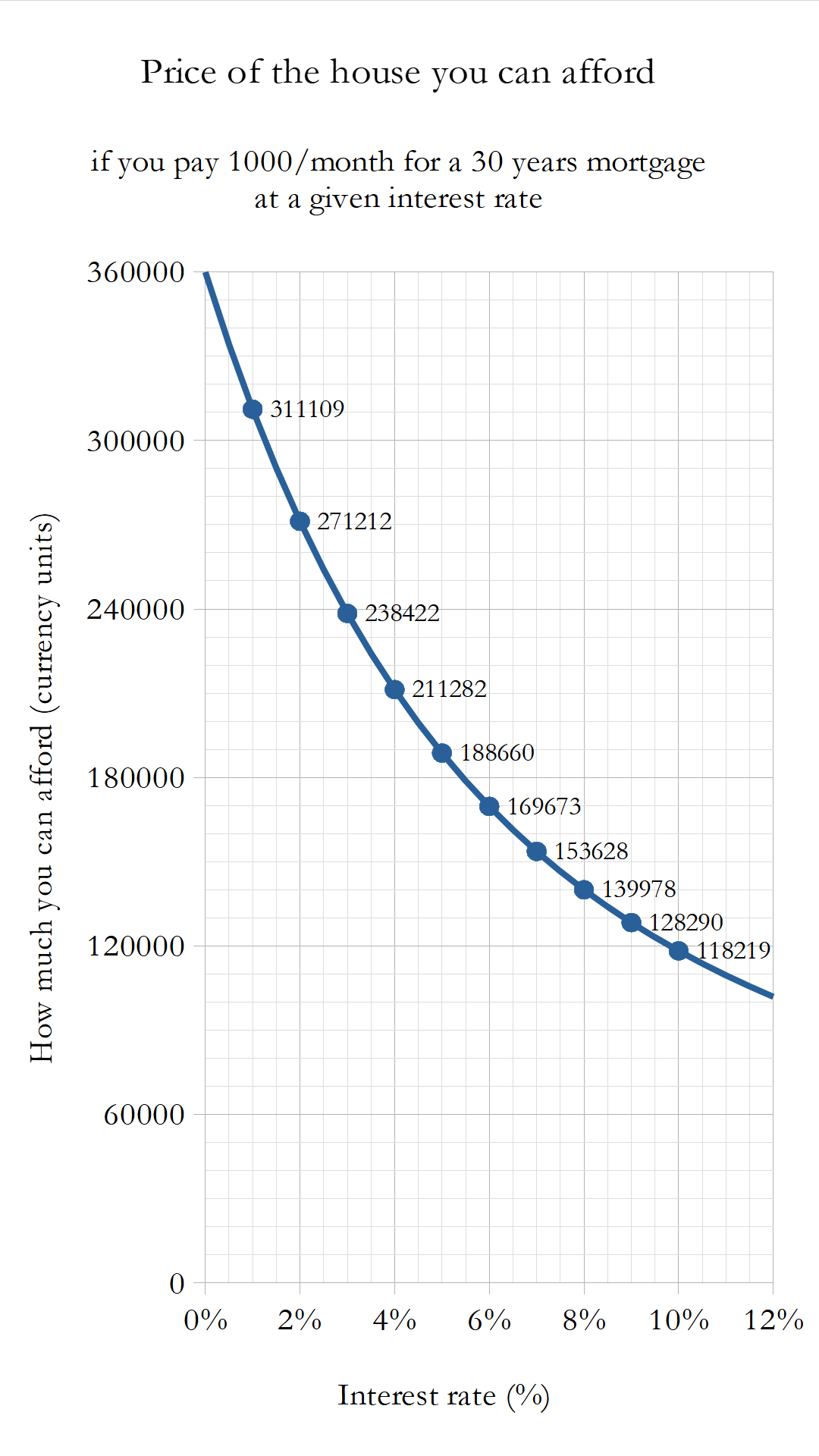

Wow. This is pretty awesome. In the 80s, rates got up to about 16%. Would be interesting to see the chart expanded to go that high.

hmiamid OP t1_irfxglg wrote

There you go up to 20%.

{kind=link}

Awkward_Ostrich_4275 t1_irg15ee wrote

Edit: it’s been fixed

The 10% rate in your two graphs don’t match up. In your post, it’s 118k on Y and in this image it’s 160k.

hmiamid OP t1_irg3zy9 wrote

So sorry about that. I played a bit with the numbers and forgot to change. I put the original parameters. So yes. It goes down a lot more.

TheOtherSomeOtherGuy t1_irijah1 wrote

You really need to use commas in your number formatting

Doctor_Kat t1_irgemyj wrote

Wow. At 16% your paying $360k over the life of the loan for an $80k house.

hmiamid OP t1_irgh9w7 wrote

That's why the house prices in the 70-80s (around that time) were so low. We were actually better off a few years ago than in the past if we're looking at total mortgage payments in terms of years of median income.

Hodorous t1_irikhu3 wrote

In 70's/80's wages increased at much higher rate also(about 6% in US and over 10% in some European countries).

PryomancerMTGA t1_irhi2ms wrote

But the house appreciated as well. My parents got a $25k house in the early '70s, it worth $400k+ now.

ac9116 t1_iri4pqb wrote

The lower interest rates also had an impact on said appreciation

No_Breakfast1204 t1_irow1tc wrote

Exactly! When they say "asset bubble" fueled by low interest rates, that's a classic example.

lolubuntu t1_irlypt8 wrote

https://www.inflationtool.com/us-dollar/1970-to-present-value

25 x 7.7 = 192.5

So overall while the nominal price is up ~16x, the 'real' price is only ~2x higher after factoring in inflation.

Yeah, 400 is worth more than 200, but it's not night/day different. You would likely end up in the same (or better) living in a small place and tossing A LOT of money into stocks. The DJIA was at ~750 in 1970. It's presently at ~30,000, which is 40x higher.

PryomancerMTGA t1_irm0ewh wrote

First a technicality, home ownership is a leveraged investment that also provides several tax benefits that offset Dow index investments advantages. So it wouldn't be calculated a a 2x roi over the time period and was likely cash positive relative to renting before they sold it.

Second and most importantly, would you really advise a couple parents to rent rather than own? Home ownership and paying a mortgage has significant advantages over renting.

lolubuntu t1_irm3zb7 wrote

>First a technicality, home ownership is a leveraged investment

You can leverage stocks as well, though not as aggressively. Though calls are a thing.

>that also provides several tax benefits that offset Dow index investments advantages. So it wouldn't be calculated a a 2x roi over the time period and was likely cash positive relative to renting before they sold it.

Depends on income.

If you're in a lower income tax bracket (under $160,000) it makes less sense because the tax benefits are lower.

If you're high income and in a state like California, it makes more sense as your marginal tax rate is around 50%.

BUT this assumes that owning a house has 0 impact on income. There are studies showing that when controlling for education and a few other factors, home ownership reduces income. People are less likely to job hop. "look I saved $100k on rent the last 10 years" sounds kind of stupid if you missed out on $500k in income AND you opted for 2-4x the square footage you otherwise would have... and you spent half your free time mowing, cleaning gutters, painting, etc.

Also, taxes ARE a thing. Using a 1.5% tax rate each year, in the short to mid-run you can end up paying almost as much on property tax as you would on rent overall in A LOT of places.

This also applies on the back end if you ever try to realize appreciation as well, though there are SOME exceptions to that if you lived in a residence 2/5 years.

PryomancerMTGA t1_irm4vdc wrote

That's a really interesting point on home ownership having a negative impact on income. That's a really good point.

I wasn't aware of anywhere that had property taxes equivalent to rent. I'll have to look into that.

As you have pointed out home ownership decisions can get complicated. It was the right decision for them, but I'm the current market with avg home prices in the $500 k range and mortgage rates like they are maybe not buying makes sense (Dow scares me now too).

lolubuntu t1_irm7r8v wrote

Don't get me wrong, I wouldn't mind going back in time to 2020 and tossing some cash down and buying a house. Timing the market is hard though.

Home ownership as a FORCED savings plan has some benefits though - namely that it forces undisciplined people to toss $$$ into something other than new cars and booze.

It's just that all BS considered it's often a wash vs just putting money in an index fund.

And you would likely end up ahead, living in a tiny shoebox apartment and chasing $$$. 5 years at a FAANG banking (net of taxes) $100-200k a year is enough to basically buy a house, cash.

Home ownership is kind of fetishized at this point. It feels almost like the same level of circle jerk as it was back in 2006... though I could be off.

I'll probably buy a house when I'm sick of the rat race and decide to semi-retire (aka have enough $$$ to retire outright but want more spending $$$, something to do and the prestige of being a "semi-retired 30-something year old college professor" over just being unemployed).

No_Breakfast1204 t1_irow6m7 wrote

You sound like a real estate agent.

Sartres_Roommate t1_iri4lnj wrote

Yeah, but that is 50, not 30, years

PryomancerMTGA t1_irjdhoc wrote

Wow really, I guess it's totally meaningless then.

Sartres_Roommate t1_irkd0qk wrote

Wow, you really jumped right to the hyperbolic strawman. But let's dig on that.

A. My parents bought a house in '83 for roughly $160k and made massive capital improvements on it over 30 years and then sold it in 2015 for about $250k. The value doesn't always skyrocket, a large part of that has to with specific economic growth in the location, location, location

B. I bought a place in '99 for $120k and it sold two years ago for $290k (we sold it 10 years ago)...the location became a booming area of growth.

C. The main point is those extra 20 years your parents had that house is likely the majority of the appreciation in value. Housing overall has been on an unsustainable rocket ride for the last 20 years, even WITH the 2008 crash, and the last 2 years have been even more batshit insane.

And lastly the specifics of early to mid 70s was a market low AND right as the rampant inflation of the late 70s/early 80s kicked in. There is nothing average about your parents particular housing appreciations experience. Historically they are outliers.

And that is a a very important thing to understand. The 2008 crash was partially driven by the fallacy that home ownership was like a guaranteed profit generating machine; buy more than you can afford because if payments becomes an issue you can just sell in 2 years for 160% of what you paid for it.

randomthad69 t1_irlxtg5 wrote

My parents bought a house for100k it sold for 720 25 years later

sevargmas t1_irisigm wrote

Is this adjusted for inflation?

burn-it-all- t1_irrdlzm wrote

Awesome!! This is a great chart.

Sheamus_1852 t1_irghtd0 wrote

And the average US home price was 68k at the interest peak in 1981. It’s 348k today.

girhen t1_irhjhtu wrote

For the record, 68k in 1981 is about $222k today, and $1,000 was about $3,260.

Not saying that wiped it out - housing prices are still a bit over 50% more expensive today after inflation adjustment. Just putting context behind numbers.

Sheamus_1852 t1_iri2zrj wrote

Thank you for doing the math, I was being lazy.

Average salary in 1981 was 47,720, 2022 it’s 53,490. 47,720 adjusted for inflation to 2022 would be 155,481. People in 1981 had almost 3x the buying power of people in 2022.

Edit - average salary in 1981 was 10,495. 47,720 is already adjusted for inflation.

There is also the exponential growth law. The greater the number, the bigger the impact of APR changes. A house at 68k’s annual interest. 7.5% = 5100 10% = 6800 Difference of 1700

A house at 348k: 7.5% = 26100 10% = 34800 Difference of 8700

This is why interest is a larger impact now. When houses are 68k going up 2.5% is not a massive impact. That’s $142 on a monthly payment. You can penny pinch to make that happen. At 348k a 2.5% hike is $725 monthly. There’s not many who can penny pinch to get around that. These are in year dollar values because that is how the impact would be felt.

Housing prices have far outpaced wages leaving minor interest rate increases to cause massive swings in profitability. There is always the chance to refinance but we’ve all gotta wait on that.

TiredPistachio t1_iri9k01 wrote

You salary info at the top is wrong. Those numbers are already inflation adjusted

Sheamus_1852 t1_irib6bd wrote

Thanks for the heads up. I edited the comment.

857477459 t1_irgo4jp wrote

This is why all those posts about how much less houses used to cost need to be taken with a grain of salt. House prices are so high in large part because interest rates were so low for so long.

Negs01 t1_irhn5mt wrote

Indeed, construction costs have likely increased for various reasons, but I would bet that low interest rates along with other subsidies (lowering FHA standards for example) have been the primary drivers of increased home costs.

​

I'm curious how much the price has increased in terms of square feet though. Average home price has gone up, but so has average home size.

​

This is a little dated, but assuming the trend did not reverse, median home sizes have increased at least 66% since the early 1970s.

Neat-Programmer2722 t1_irigxzi wrote

In my area houses and affordable housing was not being built at a proper rate due to a lot of factors but yes labor material costs were part of that.

Now the prices are so high there is a housing build rush however there is an extreme shortage of labor and extreme shortage of housing. Supply and demand.

Sartres_Roommate t1_iri4tjq wrote

That is a gross oversimplification at best....and that is being generous.

izzie90 t1_irijcdh wrote

My first house (townhouse) out of college in 1984 was $62k at 14.5% mortgage in capital district NY. We sold it 5 yrs later for 90k. That buyer sold it 20 yrs later in 2019 for $194k. Zillow has it estimated now at $258k

cepegma t1_irie1ib wrote

What's certain is that the interest will stay high at least during the 2 years to come. Very likely they will continue to go up.

Viewing a single comment thread. View all comments