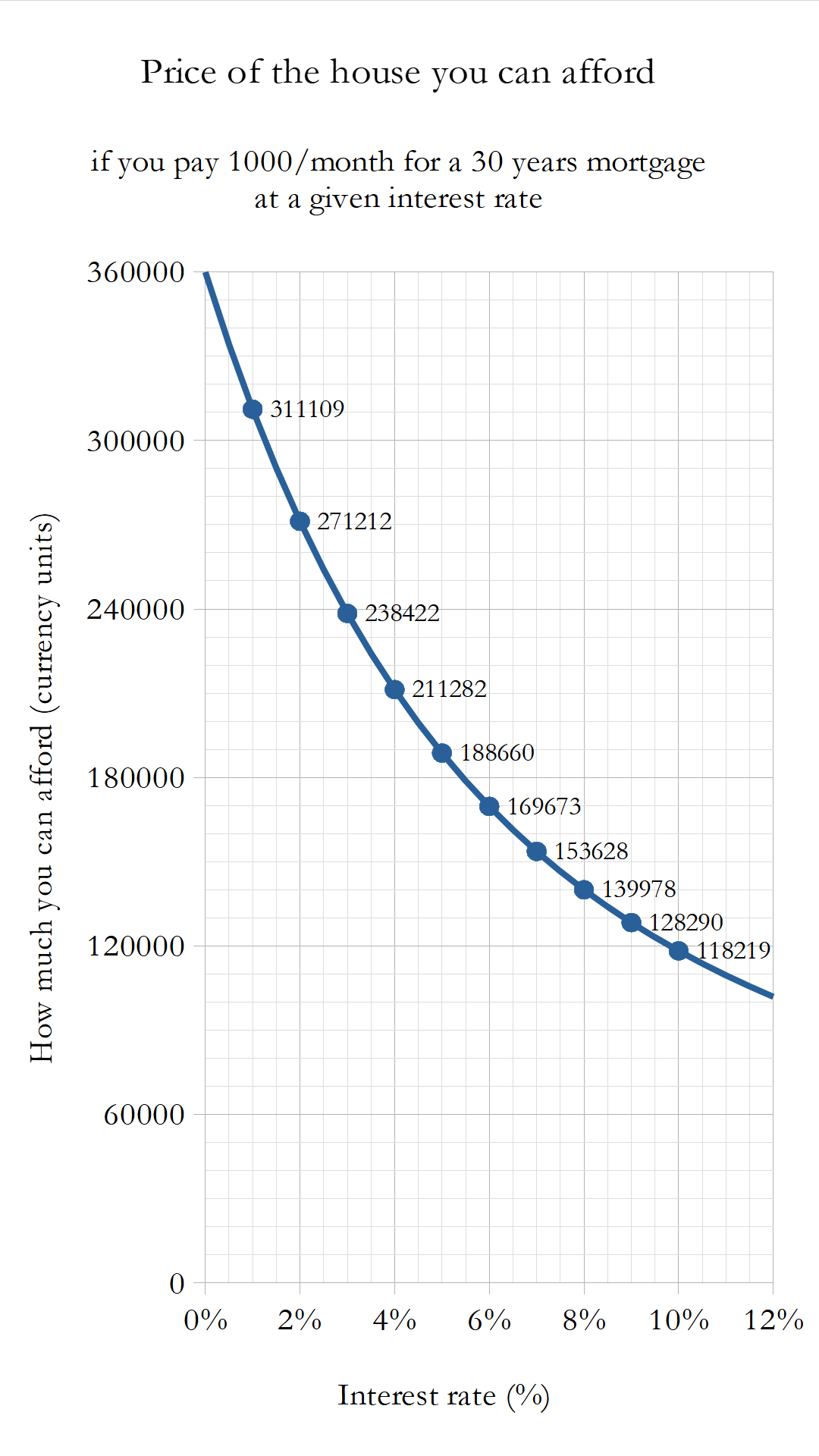

[OC] House price you can afford by paying 1000/month for 30 years vs. interest rate

[OC] House price you can afford by paying 1000/month for 30 years vs. interest rateSubmitted by hmiamid t3_xy7qym in dataisbeautiful

squeevey t1_irfxu4f wrote

Don't forget to subtract your downpayment.

padizzledonk t1_irg1a71 wrote

Don't forget to add back in to the monthly payment property taxes and insurance costs lol

squeevey t1_irg1qbs wrote

Those costs don't compound.

padizzledonk t1_irg8594 wrote

But it's part of the monthly cost of buying a home.

If you can afford a $1000 a month payment you really can't afford a $1000 a month mortage payment because your monthly payment is more Like 1600 a month figuring taxes and insurance(in my case....well, mine is more like 1200 but whatever)

I bring this up because it effects the total cost of the home you can actually afford

6700 is cheap in NJ, I have friends that pay 2x and 3x that....their tax bill alone is about a 1000-1500 a month

It just sets the entry bar lower

I get what you are trying to illustrate though- that the interest rate effects the overall cost far more than people realize....well, people who haven't lived under anything but the unsustainable and unrealistic interest rates of the last 20 or so years

thelandsman55 t1_irg9bf8 wrote

I feel like this is a little misleading because property taxes also reduce the value of homes all else being equal, so the costs are more likely to be passed on via reduced sale price than increased monthly payments.

hmiamid OP t1_irg51qj wrote

Interesting (no pun intended). I suppose we pay more downpayment at a high interest rate. Can we actually afford to save more in a high interest rate environment to prepare for a downpayment?

squeevey t1_irg8reg wrote

Well, some were already saving regularly in preparation to purchase a house when housing prices skyrocketed. So it didn't seem prudent make rushed purchases, especially when you didn't have the EXTRA cash (on top of the down payment) to go above your proposed house price.

Some people are sitting on cash at the moment, waiting for the right time.

My point though is that with ANY compound interest chart, the chart only represents the LOAN you took, not necessarily the price of the house.

You may be able to afford 300,000 house when you chop $50K off the principle. It's all about how the various maths work for your specific situation.

Tak_Galaman t1_iria871 wrote

Ooo yeah I was trying to figure out why this was so far off from my reality. It's because this chart is about the mortgage you can afford not the total house price.

pivantun t1_irgd8h9 wrote

I think it's the other way around: When interest rates are low, house prices get inflated, and so downpayments go up.

Viewing a single comment thread. View all comments