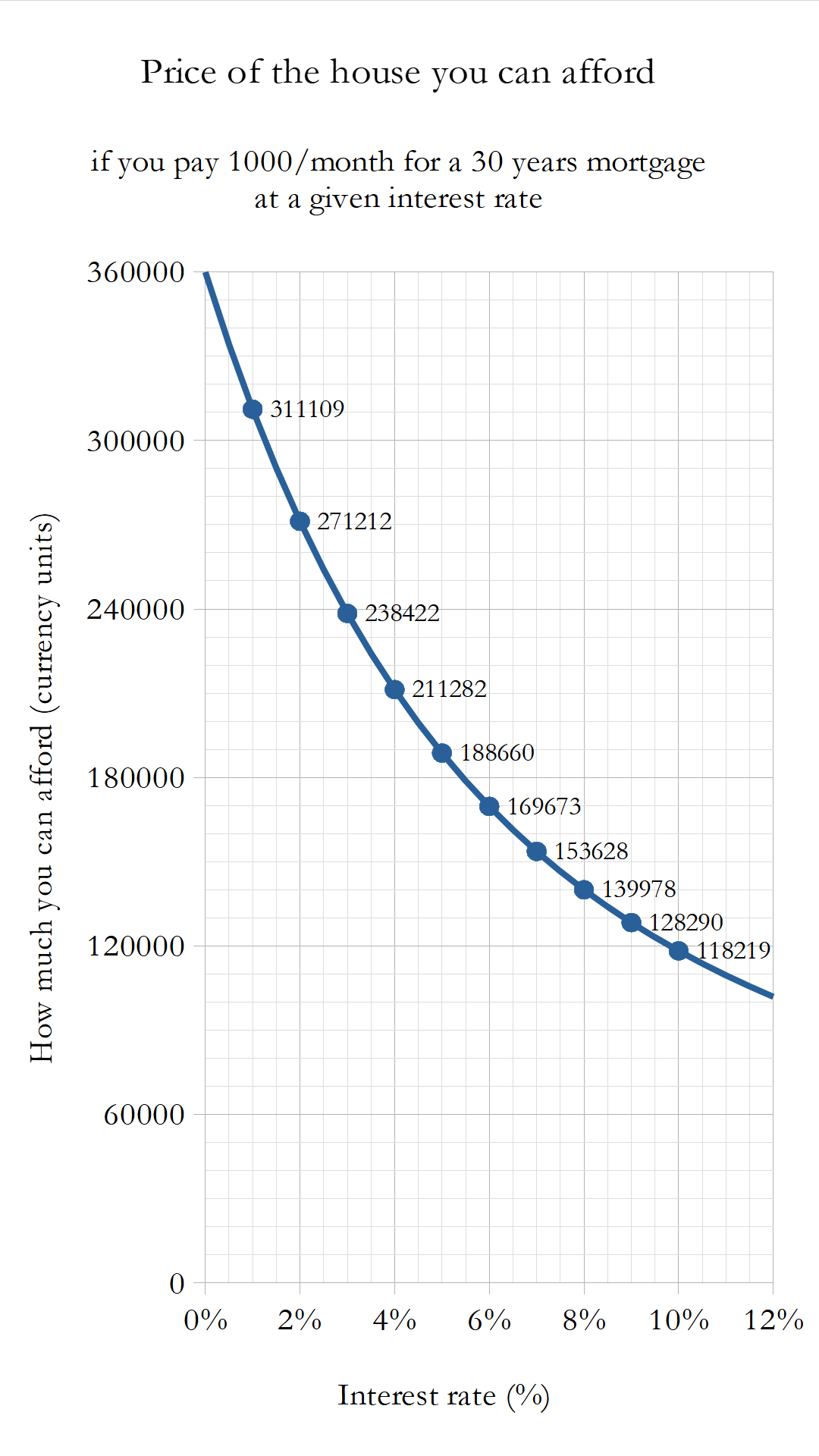

[OC] House price you can afford by paying 1000/month for 30 years vs. interest rate

[OC] House price you can afford by paying 1000/month for 30 years vs. interest rateSubmitted by hmiamid t3_xy7qym in dataisbeautiful

hmiamid OP t1_iribryz wrote

Reply to comment by julietOscarEch0 in [OC] House price you can afford by paying 1000/month for 30 years vs. interest rate by hmiamid

The point is how fast the curve drops from low mortgage rates to high ones. This in turn drives the house prices down because of lower purchasing power. And that's for everyone. It won't be half though because every buyer is not a new buyer. Remortgaging is in some countries (like the UK) a necessity too as they are mostly 5 yr fixed then go to SVR. Of course if you lock a 30yr low rate, you don't care about all this. But it's not the case of everyone and some countries will be more affected than others.

julietOscarEch0 t1_irictdc wrote

But what do you think your numbers represent? US mortgage rates already went from 3 to 6/7 and we're not seeing anything like the drop you show. I contend that's because your analysis is naive with respect to inflation.

Regarding the UK market sure, but then the impact on 30 years fixed repayments is irrelevant because you can't fix for 30 years. Again, the wage/house price picture in 5 years (actually less since many people fix for 2) cannot be ignored.

hmiamid OP t1_irihdpf wrote

- you don't really expect the market to crash the day after the interest rates rise. Its a slow progress.

- how do you think UK banks calculate people's affordability then?

julietOscarEch0 t1_iril2ei wrote

UK bank affordability test already bake in a component of resilience to rate rises and the binding constraint for most people is an income multiple limit or raising a deposit. As such affordability has a lower dependence on rates than you might expect(and certainly nothing like your model). Probably the biggest impact so far is banks starting to withdraw 95% LTV deals.

So when do you expect the 30% drop in prices? I assume you have sold all property and found a way to short real estate since you seem to think the outcome is so certain?

Viewing a single comment thread. View all comments